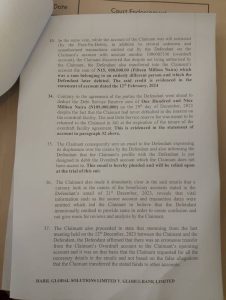

Haril Global Solutions Limited has asked the Federal Capital Territory High Court to order Globus Bank Limited to pay it N10 billion in general damages for an alleged breach of loan contract, among other issues.

This relief is outlined in its writ of summons instituted against the bank in suit number CV/1456/2024.

The claimant contends that the bank allegedly carried out multiple transactions on its account without the company’s knowledge or authorization, thereby failing to comply with the terms and conditions of the loan agreement.

The applicant’s lawyer, Pelumi Olajengbesi Esq., stated that despite the defendant breaching the contract terms with his client, it wrote to Access Bank, Fidelity Bank, and Wema Bank, allegedly misrepresenting facts.

He stated that as a result, the respective banks placed a “post no debit” on all his client’s accounts held with them.

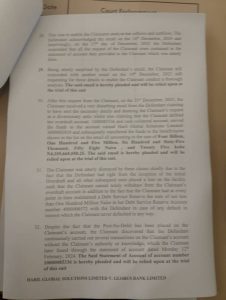

In the claimant’s statement on oath, deposed by Oluwaseun Onobun, a Director at Haril Global, he explained that on December 7, 2021, Globus Bank sent a letter to his company offering an overdraft loan facility of N500,000,000.00 to augment the claimant’s working capital, with a tenor of one year.

He stated that the offer letter was duly signed , signifying the company’s acceptance of the offer from Globus.

The witness indicated that the express terms and conditions of the overdraft loan facility specified that the loan was provided at an interest rate of 16% per annum, and Globus was to maintain a Debt Service Reserve Account (DSRA) funded with at least two months’ interest cover for the duration of the facility.

Furthermore, the offer letter stipulated that if funds were withdrawn from the DSRA to cover a shortfall in debt service, the company was required to restore the credit balance of the DSRA to an amount equal to two months’ interest within two days. Failure to do so would constitute an event of default under the facility.

He argued that due to the longstanding cordial relationship between the claimant and Globus Bank, and the fact that the claimant never defaulted on the contract terms, the defendant offered to increase the overdraft loan facility from N500,000,000 to N1,000,000,000 on July 14, 2022, to meet the claimant’s operational cash flow requirements for a year.

He further stated that after the completion of the initial one year loan arrangement and the smooth business relationship, the facility was increased to N5,000,000,000, then to N7,000,000,000, and finally to N8,000,000,000 in August 2023 at various times.

He maintained that the claimant, from 2021 to 2023, when the overdraft loan facility was initiated and reviewed with increments, promptly paid all rates, charges, and interest, including N734,215,998.84 as interest on the facility between April 2023 and January 2024.

He stated, that “however, to the claimant’s dismay, on November 22, 2023, the claimant noticed a significant reduction in the overdraft with an available balance from over N4,000,000,000 from the N8,000,000,000 duly granted to a surprising N223,000,000,” he submitted.

He said that on December 13, 2023, following inquiries, Globus Bank sent a doctored statement of account dated December 13, 2023, containing transactions the claimant was unaware of.

He stated that the claimant responded to an email from the defendant on December 14, 2023, seeking clarity and reports on the overdraft and collection accounts.

The claimant requested detailed information on all debit and credit transactions, including transactions IDs, dates and amounts noting missing information in the defendant’s December 21, 2023 email, which suggested intentional omission to create confusion.

He stated that Globus Bank later confirmed an erroneous transfer occurred from the claimant’s overdraft account to the claimant’s operating account.

He said that it was based on the banks disclosure of erroneous transfers that the claimant requested for the details of the transaction via emails.

“At the referenced meeting, the defendant promised to restore the claimant’s Corporate Internet Banking profiles to enable the claimant to manage their liquidation, view their balance, and download statutory reports (the same reports the defendant refused to send to the claimant), but the defendant failed to do so,” he submitted.

He said that amidst these developments, Globus Bank continued collecting undue interest from the claimant despite the claimant being unable to conduct business due to restrictions placed on their account due to suspicious transactions.

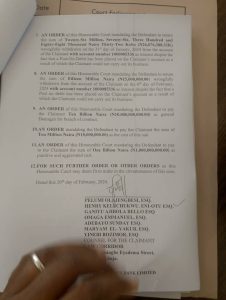

“As a result of the ‘Post-No-Debit’ placed on the claimant’s accounts, the claimant has lost the business goodwill of her clients and has incurred a gross loss of Ten Billion Naira (N10,000,000,000.00) due to the inability to conduct business with all accounts held with the defendant, Access Bank, Fidelity Bank, and Wema Bank,” he stated.

The claimant subsequently urged the Court to impose N10 billion in damages on Globus Bank while ordering the bank to return the several millions withdrawn from its accounts.

The claimant’s lawyer argued that the bank’s claims of erroneous transactions are doubtful, as the bank had imposed restrictions on the loan facility from the beginning, preventing his client from solely withdrawing from the claimant’s overdraft account.

He added that the claimant had consistently maintained a Debt Service Reserve fee of not less than One Hundred Million Naira with the bank as a precaution against any default, which his client never committed.

In response, the bank denied the allegations made by the claimant.

In the bank’s counter affidavit , deposed by Tamunosiki Wakama (a litigation clerk), it was stated that the relief sought by the applicant is not in the interest of justice and should be dismissed.

The court has scheduled January 13 and 14, 2025, for the hearing of the case.

Haril Global Solutions Limited has asked the Federal Capital Territory High Court to order Globus Bank Limited to pay it N10 billion in general damages for an alleged breach of loan contract, among other issues.

This relief is outlined in its writ of summons instituted against the bank in suit number CV/1456/2024.

The claimant contends that the bank allegedly carried out multiple transactions on its account without the company’s knowledge or authorization, thereby failing to comply with the terms and conditions of the loan agreement.

The applicant’s lawyer, Pelumi Olajengbesi Esq., stated that despite the defendant breaching the contract terms with his client, it wrote to Access Bank, Fidelity Bank, and Wema Bank, allegedly misrepresenting facts.

He stated that as a result, the respective banks placed a “post no debit” on all his client’s accounts held with them.

In the claimant’s statement on oath, deposed by Oluwaseun Onobun, a Director at Haril Global, he explained that on December 7, 2021, Globus Bank sent a letter to his company offering an overdraft loan facility of N500,000,000.00 to augment the claimant’s working capital, with a tenor of one year.

He stated that the offer letter was duly signed , signifying the company’s acceptance of the offer from Globus.

The witness indicated that the express terms and conditions of the overdraft loan facility specified that the loan was provided at an interest rate of 16% per annum, and Globus was to maintain a Debt Service Reserve Account (DSRA) funded with at least two months’ interest cover for the duration of the facility.

Furthermore, the offer letter stipulated that if funds were withdrawn from the DSRA to cover a shortfall in debt service, the company was required to restore the credit balance of the DSRA to an amount equal to two months’ interest within two days. Failure to do so would constitute an event of default under the facility.

He argued that due to the longstanding cordial relationship between the claimant and Globus Bank, and the fact that the claimant never defaulted on the contract terms, the defendant offered to increase the overdraft loan facility from N500,000,000 to N1,000,000,000 on July 14, 2022, to meet the claimant’s operational cash flow requirements for a year.

He further stated that after the completion of the initial one year loan arrangement and the smooth business relationship, the facility was increased to N5,000,000,000, then to N7,000,000,000, and finally to N8,000,000,000 in August 2023 at various times.

He maintained that the claimant, from 2021 to 2023, when the overdraft loan facility was initiated and reviewed with increments, promptly paid all rates, charges, and interest, including N734,215,998.84 as interest on the facility between April 2023 and January 2024.

He stated, that “however, to the claimant’s dismay, on November 22, 2023, the claimant noticed a significant reduction in the overdraft with an available balance from over N4,000,000,000 from the N8,000,000,000 duly granted to a surprising N223,000,000,” he submitted.

He said that on December 13, 2023, following inquiries, Globus Bank sent a doctored statement of account dated December 13, 2023, containing transactions the claimant was unaware of.

He stated that the claimant responded to an email from the defendant on December 14, 2023, seeking clarity and reports on the overdraft and collection accounts.

The claimant requested detailed information on all debit and credit transactions, including transactions IDs, dates and amounts noting missing information in the defendant’s December 21, 2023 email, which suggested intentional omission to create confusion.

He stated that Globus Bank later confirmed an erroneous transfer occurred from the claimant’s overdraft account to the claimant’s operating account.

He said that it was based on the banks disclosure of erroneous transfers that the claimant requested for the details of the transaction via emails.

“At the referenced meeting, the defendant promised to restore the claimant’s Corporate Internet Banking profiles to enable the claimant to manage their liquidation, view their balance, and download statutory reports (the same reports the defendant refused to send to the claimant), but the defendant failed to do so,” he submitted.

He said that amidst these developments, Globus Bank continued collecting undue interest from the claimant despite the claimant being unable to conduct business due to restrictions placed on their account due to suspicious transactions.

“As a result of the ‘Post-No-Debit’ placed on the claimant’s accounts, the claimant has lost the business goodwill of her clients and has incurred a gross loss of Ten Billion Naira (N10,000,000,000.00) due to the inability to conduct business with all accounts held with the defendant, Access Bank, Fidelity Bank, and Wema Bank,” he stated.

The claimant subsequently urged the Court to impose N10 billion in damages on Globus Bank while ordering the bank to return the several millions withdrawn from its accounts.

The claimant’s lawyer argued that the bank’s claims of erroneous transactions are doubtful, as the bank had imposed restrictions on the loan facility from the beginning, preventing his client from solely withdrawing from the claimant’s overdraft account.

He added that the claimant had consistently maintained a Debt Service Reserve fee of not less than One Hundred Million Naira with the bank as a precaution against any default, which his client never committed.

In response, the bank denied the allegations made by the claimant.

In the bank’s counter affidavit , deposed by Tamunosiki Wakama (a litigation clerk), it was stated that the relief sought by the applicant is not in the interest of justice and should be dismissed.

The court has scheduled January 13 and 14, 2025, for the hearing of the case.

Haril Global Solutions Limited has asked the Federal Capital Territory High Court to order Globus Bank Limited to pay it N10 billion in general damages for an alleged breach of loan contract, among other issues.

This relief is outlined in its writ of summons instituted against the bank in suit number CV/1456/2024.

The claimant contends that the bank allegedly carried out multiple transactions on its account without the company’s knowledge or authorization, thereby failing to comply with the terms and conditions of the loan agreement.

The applicant’s lawyer, Pelumi Olajengbesi Esq., stated that despite the defendant breaching the contract terms with his client, it wrote to Access Bank, Fidelity Bank, and Wema Bank, allegedly misrepresenting facts.

He stated that as a result, the respective banks placed a “post no debit” on all his client’s accounts held with them.

In the claimant’s statement on oath, deposed by Oluwaseun Onobun, a Director at Haril Global, he explained that on December 7, 2021, Globus Bank sent a letter to his company offering an overdraft loan facility of N500,000,000.00 to augment the claimant’s working capital, with a tenor of one year.

He stated that the offer letter was duly signed , signifying the company’s acceptance of the offer from Globus.

The witness indicated that the express terms and conditions of the overdraft loan facility specified that the loan was provided at an interest rate of 16% per annum, and Globus was to maintain a Debt Service Reserve Account (DSRA) funded with at least two months’ interest cover for the duration of the facility.

Furthermore, the offer letter stipulated that if funds were withdrawn from the DSRA to cover a shortfall in debt service, the company was required to restore the credit balance of the DSRA to an amount equal to two months’ interest within two days. Failure to do so would constitute an event of default under the facility.

He argued that due to the longstanding cordial relationship between the claimant and Globus Bank, and the fact that the claimant never defaulted on the contract terms, the defendant offered to increase the overdraft loan facility from N500,000,000 to N1,000,000,000 on July 14, 2022, to meet the claimant’s operational cash flow requirements for a year.

He further stated that after the completion of the initial one year loan arrangement and the smooth business relationship, the facility was increased to N5,000,000,000, then to N7,000,000,000, and finally to N8,000,000,000 in August 2023 at various times.

He maintained that the claimant, from 2021 to 2023, when the overdraft loan facility was initiated and reviewed with increments, promptly paid all rates, charges, and interest, including N734,215,998.84 as interest on the facility between April 2023 and January 2024.

He stated, that “however, to the claimant’s dismay, on November 22, 2023, the claimant noticed a significant reduction in the overdraft with an available balance from over N4,000,000,000 from the N8,000,000,000 duly granted to a surprising N223,000,000,” he submitted.

He said that on December 13, 2023, following inquiries, Globus Bank sent a doctored statement of account dated December 13, 2023, containing transactions the claimant was unaware of.

He stated that the claimant responded to an email from the defendant on December 14, 2023, seeking clarity and reports on the overdraft and collection accounts.

The claimant requested detailed information on all debit and credit transactions, including transactions IDs, dates and amounts noting missing information in the defendant’s December 21, 2023 email, which suggested intentional omission to create confusion.

He stated that Globus Bank later confirmed an erroneous transfer occurred from the claimant’s overdraft account to the claimant’s operating account.

He said that it was based on the banks disclosure of erroneous transfers that the claimant requested for the details of the transaction via emails.

“At the referenced meeting, the defendant promised to restore the claimant’s Corporate Internet Banking profiles to enable the claimant to manage their liquidation, view their balance, and download statutory reports (the same reports the defendant refused to send to the claimant), but the defendant failed to do so,” he submitted.

He said that amidst these developments, Globus Bank continued collecting undue interest from the claimant despite the claimant being unable to conduct business due to restrictions placed on their account due to suspicious transactions.

“As a result of the ‘Post-No-Debit’ placed on the claimant’s accounts, the claimant has lost the business goodwill of her clients and has incurred a gross loss of Ten Billion Naira (N10,000,000,000.00) due to the inability to conduct business with all accounts held with the defendant, Access Bank, Fidelity Bank, and Wema Bank,” he stated.

The claimant subsequently urged the Court to impose N10 billion in damages on Globus Bank while ordering the bank to return the several millions withdrawn from its accounts.

The claimant’s lawyer argued that the bank’s claims of erroneous transactions are doubtful, as the bank had imposed restrictions on the loan facility from the beginning, preventing his client from solely withdrawing from the claimant’s overdraft account.

He added that the claimant had consistently maintained a Debt Service Reserve fee of not less than One Hundred Million Naira with the bank as a precaution against any default, which his client never committed.

In response, the bank denied the allegations made by the claimant.

In the bank’s counter affidavit , deposed by Tamunosiki Wakama (a litigation clerk), it was stated that the relief sought by the applicant is not in the interest of justice and should be dismissed.

The court has scheduled January 13 and 14, 2025, for the hearing of the case.

Haril Global Solutions Limited has asked the Federal Capital Territory High Court to order Globus Bank Limited to pay it N10 billion in general damages for an alleged breach of loan contract, among other issues.

This relief is outlined in its writ of summons instituted against the bank in suit number CV/1456/2024.

The claimant contends that the bank allegedly carried out multiple transactions on its account without the company’s knowledge or authorization, thereby failing to comply with the terms and conditions of the loan agreement.

The applicant’s lawyer, Pelumi Olajengbesi Esq., stated that despite the defendant breaching the contract terms with his client, it wrote to Access Bank, Fidelity Bank, and Wema Bank, allegedly misrepresenting facts.

He stated that as a result, the respective banks placed a “post no debit” on all his client’s accounts held with them.

In the claimant’s statement on oath, deposed by Oluwaseun Onobun, a Director at Haril Global, he explained that on December 7, 2021, Globus Bank sent a letter to his company offering an overdraft loan facility of N500,000,000.00 to augment the claimant’s working capital, with a tenor of one year.

He stated that the offer letter was duly signed , signifying the company’s acceptance of the offer from Globus.

The witness indicated that the express terms and conditions of the overdraft loan facility specified that the loan was provided at an interest rate of 16% per annum, and Globus was to maintain a Debt Service Reserve Account (DSRA) funded with at least two months’ interest cover for the duration of the facility.

Furthermore, the offer letter stipulated that if funds were withdrawn from the DSRA to cover a shortfall in debt service, the company was required to restore the credit balance of the DSRA to an amount equal to two months’ interest within two days. Failure to do so would constitute an event of default under the facility.

He argued that due to the longstanding cordial relationship between the claimant and Globus Bank, and the fact that the claimant never defaulted on the contract terms, the defendant offered to increase the overdraft loan facility from N500,000,000 to N1,000,000,000 on July 14, 2022, to meet the claimant’s operational cash flow requirements for a year.

He further stated that after the completion of the initial one year loan arrangement and the smooth business relationship, the facility was increased to N5,000,000,000, then to N7,000,000,000, and finally to N8,000,000,000 in August 2023 at various times.

He maintained that the claimant, from 2021 to 2023, when the overdraft loan facility was initiated and reviewed with increments, promptly paid all rates, charges, and interest, including N734,215,998.84 as interest on the facility between April 2023 and January 2024.

He stated, that “however, to the claimant’s dismay, on November 22, 2023, the claimant noticed a significant reduction in the overdraft with an available balance from over N4,000,000,000 from the N8,000,000,000 duly granted to a surprising N223,000,000,” he submitted.

He said that on December 13, 2023, following inquiries, Globus Bank sent a doctored statement of account dated December 13, 2023, containing transactions the claimant was unaware of.

He stated that the claimant responded to an email from the defendant on December 14, 2023, seeking clarity and reports on the overdraft and collection accounts.

The claimant requested detailed information on all debit and credit transactions, including transactions IDs, dates and amounts noting missing information in the defendant’s December 21, 2023 email, which suggested intentional omission to create confusion.

He stated that Globus Bank later confirmed an erroneous transfer occurred from the claimant’s overdraft account to the claimant’s operating account.

He said that it was based on the banks disclosure of erroneous transfers that the claimant requested for the details of the transaction via emails.

“At the referenced meeting, the defendant promised to restore the claimant’s Corporate Internet Banking profiles to enable the claimant to manage their liquidation, view their balance, and download statutory reports (the same reports the defendant refused to send to the claimant), but the defendant failed to do so,” he submitted.

He said that amidst these developments, Globus Bank continued collecting undue interest from the claimant despite the claimant being unable to conduct business due to restrictions placed on their account due to suspicious transactions.

“As a result of the ‘Post-No-Debit’ placed on the claimant’s accounts, the claimant has lost the business goodwill of her clients and has incurred a gross loss of Ten Billion Naira (N10,000,000,000.00) due to the inability to conduct business with all accounts held with the defendant, Access Bank, Fidelity Bank, and Wema Bank,” he stated.

The claimant subsequently urged the Court to impose N10 billion in damages on Globus Bank while ordering the bank to return the several millions withdrawn from its accounts.

The claimant’s lawyer argued that the bank’s claims of erroneous transactions are doubtful, as the bank had imposed restrictions on the loan facility from the beginning, preventing his client from solely withdrawing from the claimant’s overdraft account.

He added that the claimant had consistently maintained a Debt Service Reserve fee of not less than One Hundred Million Naira with the bank as a precaution against any default, which his client never committed.

In response, the bank denied the allegations made by the claimant.

In the bank’s counter affidavit , deposed by Tamunosiki Wakama (a litigation clerk), it was stated that the relief sought by the applicant is not in the interest of justice and should be dismissed.

The court has scheduled January 13 and 14, 2025, for the hearing of the case.

Haril Global Solutions Limited has asked the Federal Capital Territory High Court to order Globus Bank Limited to pay it N10 billion in general damages for an alleged breach of loan contract, among other issues.

This relief is outlined in its writ of summons instituted against the bank in suit number CV/1456/2024.

The claimant contends that the bank allegedly carried out multiple transactions on its account without the company’s knowledge or authorization, thereby failing to comply with the terms and conditions of the loan agreement.

The applicant’s lawyer, Pelumi Olajengbesi Esq., stated that despite the defendant breaching the contract terms with his client, it wrote to Access Bank, Fidelity Bank, and Wema Bank, allegedly misrepresenting facts.

He stated that as a result, the respective banks placed a “post no debit” on all his client’s accounts held with them.

In the claimant’s statement on oath, deposed by Oluwaseun Onobun, a Director at Haril Global, he explained that on December 7, 2021, Globus Bank sent a letter to his company offering an overdraft loan facility of N500,000,000.00 to augment the claimant’s working capital, with a tenor of one year.

He stated that the offer letter was duly signed , signifying the company’s acceptance of the offer from Globus.

The witness indicated that the express terms and conditions of the overdraft loan facility specified that the loan was provided at an interest rate of 16% per annum, and Globus was to maintain a Debt Service Reserve Account (DSRA) funded with at least two months’ interest cover for the duration of the facility.

Furthermore, the offer letter stipulated that if funds were withdrawn from the DSRA to cover a shortfall in debt service, the company was required to restore the credit balance of the DSRA to an amount equal to two months’ interest within two days. Failure to do so would constitute an event of default under the facility.

He argued that due to the longstanding cordial relationship between the claimant and Globus Bank, and the fact that the claimant never defaulted on the contract terms, the defendant offered to increase the overdraft loan facility from N500,000,000 to N1,000,000,000 on July 14, 2022, to meet the claimant’s operational cash flow requirements for a year.

He further stated that after the completion of the initial one year loan arrangement and the smooth business relationship, the facility was increased to N5,000,000,000, then to N7,000,000,000, and finally to N8,000,000,000 in August 2023 at various times.

He maintained that the claimant, from 2021 to 2023, when the overdraft loan facility was initiated and reviewed with increments, promptly paid all rates, charges, and interest, including N734,215,998.84 as interest on the facility between April 2023 and January 2024.

He stated, that “however, to the claimant’s dismay, on November 22, 2023, the claimant noticed a significant reduction in the overdraft with an available balance from over N4,000,000,000 from the N8,000,000,000 duly granted to a surprising N223,000,000,” he submitted.

He said that on December 13, 2023, following inquiries, Globus Bank sent a doctored statement of account dated December 13, 2023, containing transactions the claimant was unaware of.

He stated that the claimant responded to an email from the defendant on December 14, 2023, seeking clarity and reports on the overdraft and collection accounts.

The claimant requested detailed information on all debit and credit transactions, including transactions IDs, dates and amounts noting missing information in the defendant’s December 21, 2023 email, which suggested intentional omission to create confusion.

He stated that Globus Bank later confirmed an erroneous transfer occurred from the claimant’s overdraft account to the claimant’s operating account.

He said that it was based on the banks disclosure of erroneous transfers that the claimant requested for the details of the transaction via emails.

“At the referenced meeting, the defendant promised to restore the claimant’s Corporate Internet Banking profiles to enable the claimant to manage their liquidation, view their balance, and download statutory reports (the same reports the defendant refused to send to the claimant), but the defendant failed to do so,” he submitted.

He said that amidst these developments, Globus Bank continued collecting undue interest from the claimant despite the claimant being unable to conduct business due to restrictions placed on their account due to suspicious transactions.

“As a result of the ‘Post-No-Debit’ placed on the claimant’s accounts, the claimant has lost the business goodwill of her clients and has incurred a gross loss of Ten Billion Naira (N10,000,000,000.00) due to the inability to conduct business with all accounts held with the defendant, Access Bank, Fidelity Bank, and Wema Bank,” he stated.

The claimant subsequently urged the Court to impose N10 billion in damages on Globus Bank while ordering the bank to return the several millions withdrawn from its accounts.

The claimant’s lawyer argued that the bank’s claims of erroneous transactions are doubtful, as the bank had imposed restrictions on the loan facility from the beginning, preventing his client from solely withdrawing from the claimant’s overdraft account.

He added that the claimant had consistently maintained a Debt Service Reserve fee of not less than One Hundred Million Naira with the bank as a precaution against any default, which his client never committed.

In response, the bank denied the allegations made by the claimant.

In the bank’s counter affidavit , deposed by Tamunosiki Wakama (a litigation clerk), it was stated that the relief sought by the applicant is not in the interest of justice and should be dismissed.

The court has scheduled January 13 and 14, 2025, for the hearing of the case.

Haril Global Solutions Limited has asked the Federal Capital Territory High Court to order Globus Bank Limited to pay it N10 billion in general damages for an alleged breach of loan contract, among other issues.

This relief is outlined in its writ of summons instituted against the bank in suit number CV/1456/2024.

The claimant contends that the bank allegedly carried out multiple transactions on its account without the company’s knowledge or authorization, thereby failing to comply with the terms and conditions of the loan agreement.

The applicant’s lawyer, Pelumi Olajengbesi Esq., stated that despite the defendant breaching the contract terms with his client, it wrote to Access Bank, Fidelity Bank, and Wema Bank, allegedly misrepresenting facts.

He stated that as a result, the respective banks placed a “post no debit” on all his client’s accounts held with them.

In the claimant’s statement on oath, deposed by Oluwaseun Onobun, a Director at Haril Global, he explained that on December 7, 2021, Globus Bank sent a letter to his company offering an overdraft loan facility of N500,000,000.00 to augment the claimant’s working capital, with a tenor of one year.

He stated that the offer letter was duly signed , signifying the company’s acceptance of the offer from Globus.

The witness indicated that the express terms and conditions of the overdraft loan facility specified that the loan was provided at an interest rate of 16% per annum, and Globus was to maintain a Debt Service Reserve Account (DSRA) funded with at least two months’ interest cover for the duration of the facility.

Furthermore, the offer letter stipulated that if funds were withdrawn from the DSRA to cover a shortfall in debt service, the company was required to restore the credit balance of the DSRA to an amount equal to two months’ interest within two days. Failure to do so would constitute an event of default under the facility.

He argued that due to the longstanding cordial relationship between the claimant and Globus Bank, and the fact that the claimant never defaulted on the contract terms, the defendant offered to increase the overdraft loan facility from N500,000,000 to N1,000,000,000 on July 14, 2022, to meet the claimant’s operational cash flow requirements for a year.

He further stated that after the completion of the initial one year loan arrangement and the smooth business relationship, the facility was increased to N5,000,000,000, then to N7,000,000,000, and finally to N8,000,000,000 in August 2023 at various times.

He maintained that the claimant, from 2021 to 2023, when the overdraft loan facility was initiated and reviewed with increments, promptly paid all rates, charges, and interest, including N734,215,998.84 as interest on the facility between April 2023 and January 2024.

He stated, that “however, to the claimant’s dismay, on November 22, 2023, the claimant noticed a significant reduction in the overdraft with an available balance from over N4,000,000,000 from the N8,000,000,000 duly granted to a surprising N223,000,000,” he submitted.

He said that on December 13, 2023, following inquiries, Globus Bank sent a doctored statement of account dated December 13, 2023, containing transactions the claimant was unaware of.

He stated that the claimant responded to an email from the defendant on December 14, 2023, seeking clarity and reports on the overdraft and collection accounts.

The claimant requested detailed information on all debit and credit transactions, including transactions IDs, dates and amounts noting missing information in the defendant’s December 21, 2023 email, which suggested intentional omission to create confusion.

He stated that Globus Bank later confirmed an erroneous transfer occurred from the claimant’s overdraft account to the claimant’s operating account.

He said that it was based on the banks disclosure of erroneous transfers that the claimant requested for the details of the transaction via emails.

“At the referenced meeting, the defendant promised to restore the claimant’s Corporate Internet Banking profiles to enable the claimant to manage their liquidation, view their balance, and download statutory reports (the same reports the defendant refused to send to the claimant), but the defendant failed to do so,” he submitted.

He said that amidst these developments, Globus Bank continued collecting undue interest from the claimant despite the claimant being unable to conduct business due to restrictions placed on their account due to suspicious transactions.

“As a result of the ‘Post-No-Debit’ placed on the claimant’s accounts, the claimant has lost the business goodwill of her clients and has incurred a gross loss of Ten Billion Naira (N10,000,000,000.00) due to the inability to conduct business with all accounts held with the defendant, Access Bank, Fidelity Bank, and Wema Bank,” he stated.

The claimant subsequently urged the Court to impose N10 billion in damages on Globus Bank while ordering the bank to return the several millions withdrawn from its accounts.

The claimant’s lawyer argued that the bank’s claims of erroneous transactions are doubtful, as the bank had imposed restrictions on the loan facility from the beginning, preventing his client from solely withdrawing from the claimant’s overdraft account.

He added that the claimant had consistently maintained a Debt Service Reserve fee of not less than One Hundred Million Naira with the bank as a precaution against any default, which his client never committed.

In response, the bank denied the allegations made by the claimant.

In the bank’s counter affidavit , deposed by Tamunosiki Wakama (a litigation clerk), it was stated that the relief sought by the applicant is not in the interest of justice and should be dismissed.

The court has scheduled January 13 and 14, 2025, for the hearing of the case.

Haril Global Solutions Limited has asked the Federal Capital Territory High Court to order Globus Bank Limited to pay it N10 billion in general damages for an alleged breach of loan contract, among other issues.

This relief is outlined in its writ of summons instituted against the bank in suit number CV/1456/2024.

The claimant contends that the bank allegedly carried out multiple transactions on its account without the company’s knowledge or authorization, thereby failing to comply with the terms and conditions of the loan agreement.

The applicant’s lawyer, Pelumi Olajengbesi Esq., stated that despite the defendant breaching the contract terms with his client, it wrote to Access Bank, Fidelity Bank, and Wema Bank, allegedly misrepresenting facts.

He stated that as a result, the respective banks placed a “post no debit” on all his client’s accounts held with them.

In the claimant’s statement on oath, deposed by Oluwaseun Onobun, a Director at Haril Global, he explained that on December 7, 2021, Globus Bank sent a letter to his company offering an overdraft loan facility of N500,000,000.00 to augment the claimant’s working capital, with a tenor of one year.

He stated that the offer letter was duly signed , signifying the company’s acceptance of the offer from Globus.

The witness indicated that the express terms and conditions of the overdraft loan facility specified that the loan was provided at an interest rate of 16% per annum, and Globus was to maintain a Debt Service Reserve Account (DSRA) funded with at least two months’ interest cover for the duration of the facility.

Furthermore, the offer letter stipulated that if funds were withdrawn from the DSRA to cover a shortfall in debt service, the company was required to restore the credit balance of the DSRA to an amount equal to two months’ interest within two days. Failure to do so would constitute an event of default under the facility.

He argued that due to the longstanding cordial relationship between the claimant and Globus Bank, and the fact that the claimant never defaulted on the contract terms, the defendant offered to increase the overdraft loan facility from N500,000,000 to N1,000,000,000 on July 14, 2022, to meet the claimant’s operational cash flow requirements for a year.

He further stated that after the completion of the initial one year loan arrangement and the smooth business relationship, the facility was increased to N5,000,000,000, then to N7,000,000,000, and finally to N8,000,000,000 in August 2023 at various times.

He maintained that the claimant, from 2021 to 2023, when the overdraft loan facility was initiated and reviewed with increments, promptly paid all rates, charges, and interest, including N734,215,998.84 as interest on the facility between April 2023 and January 2024.

He stated, that “however, to the claimant’s dismay, on November 22, 2023, the claimant noticed a significant reduction in the overdraft with an available balance from over N4,000,000,000 from the N8,000,000,000 duly granted to a surprising N223,000,000,” he submitted.

He said that on December 13, 2023, following inquiries, Globus Bank sent a doctored statement of account dated December 13, 2023, containing transactions the claimant was unaware of.

He stated that the claimant responded to an email from the defendant on December 14, 2023, seeking clarity and reports on the overdraft and collection accounts.

The claimant requested detailed information on all debit and credit transactions, including transactions IDs, dates and amounts noting missing information in the defendant’s December 21, 2023 email, which suggested intentional omission to create confusion.

He stated that Globus Bank later confirmed an erroneous transfer occurred from the claimant’s overdraft account to the claimant’s operating account.

He said that it was based on the banks disclosure of erroneous transfers that the claimant requested for the details of the transaction via emails.

“At the referenced meeting, the defendant promised to restore the claimant’s Corporate Internet Banking profiles to enable the claimant to manage their liquidation, view their balance, and download statutory reports (the same reports the defendant refused to send to the claimant), but the defendant failed to do so,” he submitted.

He said that amidst these developments, Globus Bank continued collecting undue interest from the claimant despite the claimant being unable to conduct business due to restrictions placed on their account due to suspicious transactions.

“As a result of the ‘Post-No-Debit’ placed on the claimant’s accounts, the claimant has lost the business goodwill of her clients and has incurred a gross loss of Ten Billion Naira (N10,000,000,000.00) due to the inability to conduct business with all accounts held with the defendant, Access Bank, Fidelity Bank, and Wema Bank,” he stated.

The claimant subsequently urged the Court to impose N10 billion in damages on Globus Bank while ordering the bank to return the several millions withdrawn from its accounts.

The claimant’s lawyer argued that the bank’s claims of erroneous transactions are doubtful, as the bank had imposed restrictions on the loan facility from the beginning, preventing his client from solely withdrawing from the claimant’s overdraft account.

He added that the claimant had consistently maintained a Debt Service Reserve fee of not less than One Hundred Million Naira with the bank as a precaution against any default, which his client never committed.

In response, the bank denied the allegations made by the claimant.

In the bank’s counter affidavit , deposed by Tamunosiki Wakama (a litigation clerk), it was stated that the relief sought by the applicant is not in the interest of justice and should be dismissed.

The court has scheduled January 13 and 14, 2025, for the hearing of the case.

Haril Global Solutions Limited has asked the Federal Capital Territory High Court to order Globus Bank Limited to pay it N10 billion in general damages for an alleged breach of loan contract, among other issues.

This relief is outlined in its writ of summons instituted against the bank in suit number CV/1456/2024.

The claimant contends that the bank allegedly carried out multiple transactions on its account without the company’s knowledge or authorization, thereby failing to comply with the terms and conditions of the loan agreement.

The applicant’s lawyer, Pelumi Olajengbesi Esq., stated that despite the defendant breaching the contract terms with his client, it wrote to Access Bank, Fidelity Bank, and Wema Bank, allegedly misrepresenting facts.

He stated that as a result, the respective banks placed a “post no debit” on all his client’s accounts held with them.

In the claimant’s statement on oath, deposed by Oluwaseun Onobun, a Director at Haril Global, he explained that on December 7, 2021, Globus Bank sent a letter to his company offering an overdraft loan facility of N500,000,000.00 to augment the claimant’s working capital, with a tenor of one year.

He stated that the offer letter was duly signed , signifying the company’s acceptance of the offer from Globus.

The witness indicated that the express terms and conditions of the overdraft loan facility specified that the loan was provided at an interest rate of 16% per annum, and Globus was to maintain a Debt Service Reserve Account (DSRA) funded with at least two months’ interest cover for the duration of the facility.

Furthermore, the offer letter stipulated that if funds were withdrawn from the DSRA to cover a shortfall in debt service, the company was required to restore the credit balance of the DSRA to an amount equal to two months’ interest within two days. Failure to do so would constitute an event of default under the facility.

He argued that due to the longstanding cordial relationship between the claimant and Globus Bank, and the fact that the claimant never defaulted on the contract terms, the defendant offered to increase the overdraft loan facility from N500,000,000 to N1,000,000,000 on July 14, 2022, to meet the claimant’s operational cash flow requirements for a year.

He further stated that after the completion of the initial one year loan arrangement and the smooth business relationship, the facility was increased to N5,000,000,000, then to N7,000,000,000, and finally to N8,000,000,000 in August 2023 at various times.

He maintained that the claimant, from 2021 to 2023, when the overdraft loan facility was initiated and reviewed with increments, promptly paid all rates, charges, and interest, including N734,215,998.84 as interest on the facility between April 2023 and January 2024.

He stated, that “however, to the claimant’s dismay, on November 22, 2023, the claimant noticed a significant reduction in the overdraft with an available balance from over N4,000,000,000 from the N8,000,000,000 duly granted to a surprising N223,000,000,” he submitted.

He said that on December 13, 2023, following inquiries, Globus Bank sent a doctored statement of account dated December 13, 2023, containing transactions the claimant was unaware of.

He stated that the claimant responded to an email from the defendant on December 14, 2023, seeking clarity and reports on the overdraft and collection accounts.

The claimant requested detailed information on all debit and credit transactions, including transactions IDs, dates and amounts noting missing information in the defendant’s December 21, 2023 email, which suggested intentional omission to create confusion.

He stated that Globus Bank later confirmed an erroneous transfer occurred from the claimant’s overdraft account to the claimant’s operating account.

He said that it was based on the banks disclosure of erroneous transfers that the claimant requested for the details of the transaction via emails.

“At the referenced meeting, the defendant promised to restore the claimant’s Corporate Internet Banking profiles to enable the claimant to manage their liquidation, view their balance, and download statutory reports (the same reports the defendant refused to send to the claimant), but the defendant failed to do so,” he submitted.

He said that amidst these developments, Globus Bank continued collecting undue interest from the claimant despite the claimant being unable to conduct business due to restrictions placed on their account due to suspicious transactions.

“As a result of the ‘Post-No-Debit’ placed on the claimant’s accounts, the claimant has lost the business goodwill of her clients and has incurred a gross loss of Ten Billion Naira (N10,000,000,000.00) due to the inability to conduct business with all accounts held with the defendant, Access Bank, Fidelity Bank, and Wema Bank,” he stated.

The claimant subsequently urged the Court to impose N10 billion in damages on Globus Bank while ordering the bank to return the several millions withdrawn from its accounts.

The claimant’s lawyer argued that the bank’s claims of erroneous transactions are doubtful, as the bank had imposed restrictions on the loan facility from the beginning, preventing his client from solely withdrawing from the claimant’s overdraft account.

He added that the claimant had consistently maintained a Debt Service Reserve fee of not less than One Hundred Million Naira with the bank as a precaution against any default, which his client never committed.

In response, the bank denied the allegations made by the claimant.

In the bank’s counter affidavit , deposed by Tamunosiki Wakama (a litigation clerk), it was stated that the relief sought by the applicant is not in the interest of justice and should be dismissed.

The court has scheduled January 13 and 14, 2025, for the hearing of the case.

Related posts:

Buhari seeks approval for issuance of N10bn Commissary Notes to Kogi state

Buhari seeks approval for issuance of N10bn Commissary Notes to Kogi state

Lagos Govt approves N10bn for establishment of Aquaculture Centre

Lagos Govt approves N10bn for establishment of Aquaculture Centre

NDLEA seizes heroin, khat worth N10bn at Lagos, Kano Airports, six arrested

NDLEA seizes heroin, khat worth N10bn at Lagos, Kano Airports, six arrested

Court summons Ogun Assembly over former OPIC MD’s N10bn suit

Court summons Ogun Assembly over former OPIC MD’s N10bn suit

SEC sets limit of N10bn to be raised from digital assets

SEC sets limit of N10bn to be raised from digital assets

Ekiti govt, EKSU management owe staff N10bn, SSANU alleges

Ekiti govt, EKSU management owe staff N10bn, SSANU alleges

Reps scrap N5bn Presidential Yacht budget, increase Students loan to N10bn

Reps scrap N5bn Presidential Yacht budget, increase Students loan to N10bn

Alleged N10bn diversion: EFCC set to arraign fmr Kwara governor, Abdulfatah Ahmed

Alleged N10bn diversion: EFCC set to arraign fmr Kwara governor, Abdulfatah Ahmed

{kind=link}